The following transactions were completed by the company, providing a comprehensive overview of the various types, analysis methods, impact, reporting, and management practices associated with business transactions. This in-depth exploration delves into the intricacies of transaction processing, offering valuable insights into their significance for financial performance and stakeholder decision-making.

From understanding the different types of transactions and their purposes to examining the key metrics and indicators used in transaction analysis, this guide unravels the complexities of transaction management. It explores the impact of transactions on a company’s financial health, including its assets, liabilities, and equity, and discusses the implications for various stakeholders.

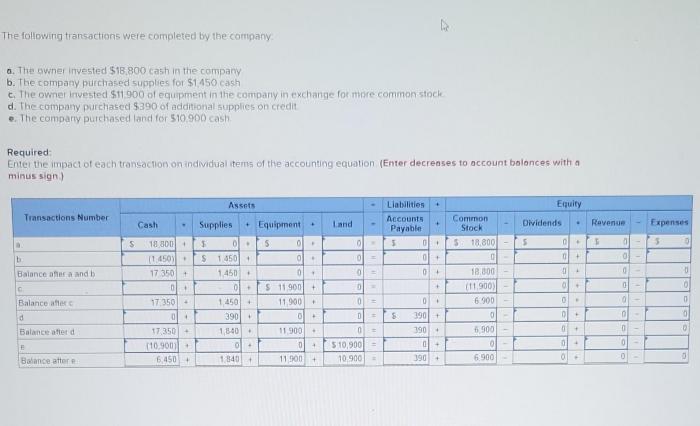

Transactions Overview: The Following Transactions Were Completed By The Company

Transactions encompass various activities that impact the financial position and performance of a company. They include:

- Revenue transactions: Generate income through the sale of goods or services.

- Expense transactions: Incur costs associated with business operations.

- Asset transactions: Acquire or dispose of tangible or intangible assets.

- Liability transactions: Create or settle obligations.

- Equity transactions: Alter the ownership or capital structure of the company.

Transaction Analysis

Transaction analysis involves examining the nature, purpose, and impact of transactions. Methods include:

- Horizontal analysis: Compares transactions over time to identify trends.

- Vertical analysis: Assesses the relative importance of transactions within a period.

- Ratio analysis: Calculates ratios using transaction data to evaluate financial performance.

Analyzing transactions is crucial for:

- Understanding the financial health of the company.

- Identifying potential areas of improvement.

- Making informed decisions about future operations.

Key metrics and indicators used in transaction analysis include:

- Gross profit margin

- Net income margin

- Return on assets (ROA)

- Return on equity (ROE)

Transaction Impact, The following transactions were completed by the company

Transactions impact the company’s financial performance by affecting its assets, liabilities, and equity. For instance:

- Revenue transactionsincrease assets (cash or accounts receivable) and equity (retained earnings).

- Expense transactionsdecrease assets (cash or inventory) and equity (retained earnings).

- Asset transactionschange the composition of assets.

- Liability transactionsaffect the amount of debt or obligations.

- Equity transactionsalter the ownership structure or capital base.

These changes can have implications for stakeholders such as investors, creditors, and management.

Transaction Reporting

Transactions are reported in financial statements, including:

- Income statement: Shows revenue and expense transactions.

- Balance sheet: Presents assets, liabilities, and equity at a specific point in time.

- Statement of cash flows: Reports cash inflows and outflows from operating, investing, and financing activities.

Regulations and standards govern transaction reporting, such as:

- Generally Accepted Accounting Principles (GAAP)

- International Financial Reporting Standards (IFRS)

Transaction Management

Best practices for transaction management include:

- Establishing clear policies and procedures.

- Implementing internal controls to prevent errors and fraud.

- Using technology to automate and streamline transactions.

- Monitoring transactions for compliance and efficiency.

Effective transaction management is crucial for ensuring the accuracy and reliability of financial information and minimizing risks.

Quick FAQs

What are the key types of transactions completed by a company?

Companies typically engage in various types of transactions, including revenue transactions (sales of goods or services), expense transactions (incurring costs), asset acquisition transactions (purchasing property or equipment), and financing transactions (raising capital).

How do companies analyze transactions?

Transaction analysis involves examining financial data to understand the nature, purpose, and impact of transactions. This can be done through techniques such as ratio analysis, trend analysis, and cash flow analysis.

What are the implications of transactions for stakeholders?

Transactions can have significant implications for stakeholders, including shareholders (impacting stock value), creditors (affecting debt偿还能力), employees (influencing compensation and benefits), and customers (impacting product availability and pricing).